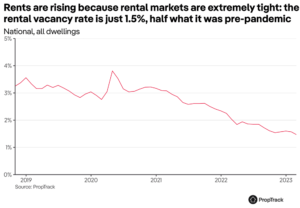

Instead, the reason rents are rising so rapidly is that rental markets are extremely tight – there just aren’t enough rentals for everyone that wants to rent.

In theory, higher interest rates lower home prices – they don’t raise rents

In theory, higher interest rates don’t affect the current supply of rental homes, nor the number of people looking for rentals.

Interest rates don’t (in theory) directly impact rents. Instead, interest rates affect home prices – which is what we are seeing at the moment. Home prices have fallen as interest rates have risen.

Interest rates can matter for rents, but only in the longer run. Higher interest rates can reduce how many homes are built, which will lower the supply of housing. But this effect takes time – around four years.

To be clear: these are intentionally simple frameworks and deliberately abstract away many important real-world details in order to focus on core concepts and mechanisms.

Maybe those simplifications matter. Maybe, in reality, higher interest rates do in fact drive higher rents through some other mechanism these models don’t capture.

So instead, let’s look at the data.

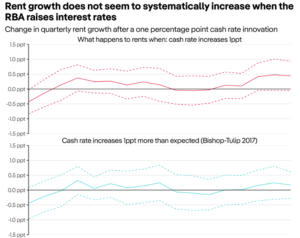

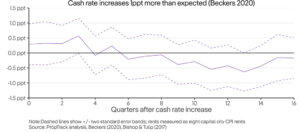

At a national level, there’s no relationship between an increase in the cash rate and higher rents

The simplest way to look at whether rates raise rents is: what happens to national average rents when the RBA raises interest rates, on average?

The top panel of the chart below shows exactly that.

The answer: not much.

There is no consistent, systematic relationship between increases in interest rates and rent growth.