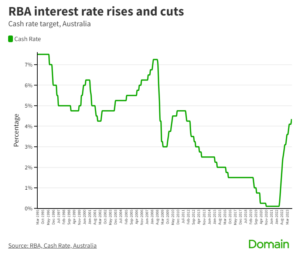

A typical borrower with a variable-rate loan can now expect an interest rate of about 6 per cent.

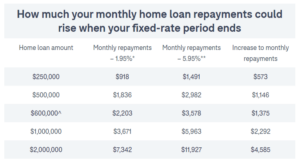

Borrowers whose fixed-rate loans are expiring this year will see their required minimum repayment amounts rise sharply based on however much their lender’s variable rate is above their low fixed rate.

“This could be a rude shock, unfortunately, as this is often the cohort who bought before, or during, COVID, and they’ve never seen cash rate increases before,” said PRD chief economist Dr Diaswati Mardiasmo.

How to prepare if your fixed rate is expiring

The most important thing people can do now, in advance, is become more informed about their situation.

“A lot of people don’t even know what interest rate their loan is today, let alone what it’s likely to move to,” said Koh. “So you have to gather all your facts and do your research now, as that process takes time.

“You should also start preparing yourself for what is to come. Will you have to dig into your savings and pay some of the principal on the loan so repayments are lower, or will you need to make changes to your lifestyle?

“If you think you’ll have to adjust your lifestyle, that generally takes people three months. So why not start now and see how it feels, and if you struggle, and think they’re changes you’re not willing to make, take decisions about alternatives?”