Homebuyer demand remains elevated despite market jitters. Picture: PropTrack

This population growth through immigration has combined with limited stock to drive rising prices, Ms. Creagh said.

“Although the significant reduction in mortgage affordability and borrowing capacities implies further price falls, the downward pressure on prices from the substantial tightening already pushed through is being countered by positive demand drivers stemming from the strong rebound in immigration, and very tight rental markets.

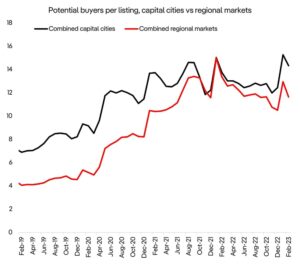

“Fewer properties are hitting the market compared to the same time last year, which is creating a more competitive buying environment and buoying home values as there remains sufficient buyer demand to help keep prices resilient.”

The ‘mortgage cliff’ impact

While there are factors driving the national market correction, a bottoming out isn’t guaranteed.

The RBA estimates about one million mortgage holders are due to face a so-called ‘mortgage cliff’ when they roll off very low fixed interest rates onto higher variable rates.

“The ‘mortgage cliff’ approaching will impact about 800,000 mortgagors in 2023 alone and this will probably lead to an uptick in supply especially in the more affordable regions,” Mr. Groves said.

Borrowers facing mortgage payment hikes have been tightening belts as a result, which has been seen in evidence showing decreased household spending nationwide.

“With consumer spending set to slow sharply, economic activity is set to weaken in the coming months as the full impact of rate rises already delivered catches up to households, businesses, and economic conditions,” Ms. Creagh said.

“If inflation pressures are more persistent than expected and the reserve bank raises interest rates further than expected the decline in prices could find a second wind, particularly if we see an increase in stock levels in the coming months, removing a pillar of support for home prices, and together with the downwards pressure from rate rises, price falls may resume.”

Has the recovery begun?

Despite stabilizing prices, mortgage rate hikes, and various economic factors coming into play, homeowners, investors and experts are all hedging their bets when predicting the property market over the next six to 12 months.

Given this uncertainty, experts say it’s likely too early to call the bottom of the market.

The path for home prices will be influenced by many variables, including the level of supply hitting the market and the trajectory of interest rates.

“If the RBA pause their tightening cycle, it’s possible the bottoming process continues, with the bounce in home prices firming and values stabilizing as uncertainty eases,” Ms. Creagh said.

“If the listings environment remains constrained, with fewer properties coming to market and low supply persists, that may continue to put a floor under prices and counter the downward pressure from the lagged effect of the higher interest rates.

“Positive demand drivers stemming from the shortages in rental supply and rebounding international migration also remain.”