It’s worth looking at the data to understand what that would mean for borrower resilience. Because it matters: a 0.5ppt decrease increases borrowing capacities by around 5%

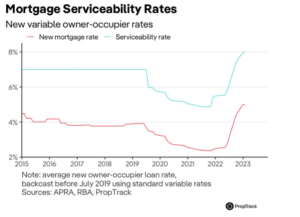

The serviceability buffer ensures financial resilience from interest rate increases

The serviceability buffer is the amount lenders add to current mortgage rates before assessing how much to lend a borrower.

Currently, new owner occupiers facing interest rates of around 5.5% must be able to afford to repay a loan if interest rates increased to 8.5%.

The serviceability buffer is designed to insulate borrowers from interest rate risk. If interest rates go up, borrowers should be able to afford to repay the loan as long as the increase is less than the buffer.

If there were no buffer, any interest rate increase would push anyone who borrowed the maximum offered into a position where they could no longer afford to make repayments.

But it is worth remembering that very few borrowers borrow their maximum – around 10% according to CBA – so most have even more resilience than described simply by the minimum buffers.

A rough recent history of the buffer and related measures is:

- December 2014: APRA standardised serviceability assessments to require a minimum 2 ppt buffer and 7% floor (a minimum serviceability rate regardless of the current interest rate)

- July 2019: the floor was removed, and the buffer increased to 2.5ppt

- November 2021: the buffer increased to 3 ppt

Over much of the past decade, the 7% floor rate was binding, meaning interest rate changes did not change borrowing capacities.

But with interest rates persistently below that level: “the gap between the 7 per cent floor and actual rates paid has become quite wide in some cases – possibly unnecessarily so” according to APRA.

In other words, the amount of resilience built into mortgages was too large and imposed a large cost in terms of restricting borrowing and locking people out of the housing market.

The current buffer covers around 95% of historical interest rate increases

The buffer protects against interest rate risk, or interest rates increasing after a borrower has taken out a loan.

No buffer can eliminate all interest rate risk since interest rates can increase indefinitely.

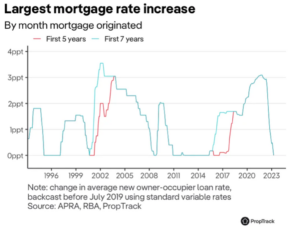

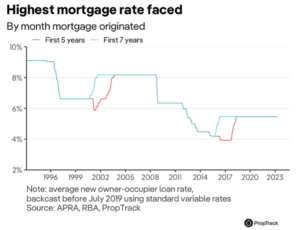

But the first 5 or 7 years of a loan are when borrowers are most susceptible to interest rate increases. This is because after this point they have generally seen their income and equity increase enough to significantly reduce the burden of mortgage repayments.