National home values increased 0.5% in the month of August, the 19th consecutive month of increase in home values. However, the pace of growth is showing clear signs of slowing.

National home values increased 0.5% in the month of August, representing the 19th consecutive month of increase in home values and slightly above the downwardly revised 0.3% increase seen through July.

However, the pace of growth is showing clear signs of slowing with the quarterly increase in national home values (1.3%) now less than half the rate of growth in the same three month period of 2023 (2.7%).

At a high level, there is still more demand for housing than available supply, but the flow of advertised supply and demand are becoming increasingly balanced. Supply levels vary markedly from region to region, with total listings in Melbourne about -25% higher than the previous five-year average, while total listings in Perth and Adelaide are down on the five-year average by more than -40%.

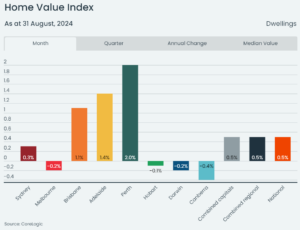

Capital growth across the cities remains diverse. Monthly gains were led by a 2.0% increase in Perth, followed by strong rises of 1.4% in Adelaide and 1.1% in Brisbane. Monthly growth in Sydney was a mild 0.3%. Four capital cities saw a monthly decline in home values, led by a -0.4% dip in Canberra, -0.2% in Melbourne and Darwin, and a mild -0.1% fall in Hobart.

Quarterly growth eased in most capital cities through winter. In Brisbane, there was a more pronounced slowdown in the quarterly growth rate between May (4.1%) and August (2.9%), suggesting an easing in demand across this increasingly less affordable market.

CoreLogic’s Head of Research, Eliza Owen, noted that while seasonality may have contributed to weaker value growth through winter, affordability constraints are a key factor behind the broader slowdown.

“The seasonally adjusted Home Value Index had a stronger result through the three months to August, at 1.7%. But this is still down from the 3.3% lift seen in the winter of 2023,” she said.

Ms Owen noted that the high levels of growth in Perth, Adelaide and Brisbane would be difficult to sustain.

“Housing values cannot keep rising at the same pace in the mid-sized capitals of Perth, Adelaide and Brisbane when affordability is becoming increasingly stretched, particularly in the context of elevated interest rates, loosening labour market conditions and cost of living pressures.”

The ongoing outperformance of ‘cheaper’ markets reiterates a strain on demand. The lower quartile of the combined capital city market, which makes up the most affordable 25% of dwellings, rose 2.7% in the three months to August, compared to a 0.3% lift across the upper quartile.

In a similar demonstration of demand being deflected towards lower price points, the quarterly change in unit values was higher than houses in five of the eight capital cities. Across the more granular SA3 markets, growth trends have also been highest in relatively affordable pockets like Canterbury in Sydney (up 13.3% in the past year), Kwinana in Perth (up 31.4%), and the Springwood – Kingston market in Brisbane (up 25.5%). More of the buyer pool may be skewed to the lower-priced segment of the market, supporting values at the more affordable end of the pricing spectrum.

The median dwelling value in Melbourne has been overtaken by Adelaide and Perth, making Melbourne’s median the third lowest among the capital city markets. The Adelaide median is now $790,800 and Perth’s is now $785,250, compared with $776,044 in Melbourne.In August, Adelaide and Perth saw increases in the median dwelling value of $13,600 and $15,300 respectively, against a -$3,100 fall in the Melbourne median.

“This is the first time that Perth’s median dwelling value has been higher than Melbourne’s since February 2015, when the city was just coming off the highs of an iron-ore boom. It is also the first time in CoreLogic’s forty-year median dwelling value series that Adelaide has had a higher median than Melbourne.”

It is worth noting that the median dwelling value is highly skewed by the portion of units in each market. Melbourne’s median is weighed down by the composition of housing in the city, where around a third of homes are units, compared with about 16% of homes in Perth and Adelaide. The median house and unit values across Perth and Adelaide are still lower than in Melbourne.

Melbourne home values have now declined for six consecutive months. Ms Owen noted there were a wide range of factors contributing to Melbourne’s softer market conditions, but it is not the only market in decline.

“The increased tax burden on investment property owners in Victoria, as shown in an annual fall in the number of investment loans secured in the state reported by the ABS, may be dissuading some demand. But it’s not the only factor at play.”

Hobart and Canberra dwelling values are also in decline, with interstate migration trends have been weak across Victoria, Tasmania and the ACT in recent years. These markets also had a stronger run-up in price growth throughout the 2010s, so it’s harder to sustain demand while interest rates are high.

“Supply is also a big factor for Victoria, where the state saw more dwelling completions over the past decade than any other state or territory. ACT also saw a spike in unit completions from 2019 to 2023, which has helped keep downward pressure on the overall dwelling market.”

Relief for renters is in sight as rent growth slows to a halt. The national CoreLogic hedonic rent index was unchanged for a second consecutive month in August, and rent values declined in Sydney for a second consecutive month.

While monthly results are subject to seasonality, the annual growth trend also shows a consistent slowdown in rent rises. Nationally, rent values were up 7.2% in the year to August, which is the lowest annual growth rate since May 2021. Annual rent growth is now slowing in every capital city market, except for Hobart, which is coming off a dip in rent values through 2023.

Ms Owen said the slowdown in rent growth is likely attributable to a combination of supply and demand factors.

“On the demand side, net overseas migration has dropped, with ABS data showing a decline from 165,000 in the March quarter of 2023 to 107,000 in December quarter, and overseas arrivals data suggests a fall in international student arrivals.”

Additionally, the latest RBA reporting on average household size showed a slight uptick, suggesting share housing or multi-generational family homes may be back on the rise in response to high rents.

“On the supply side, investor trends vary state-to-state, but nationally investor loans secured were up 10.7% in the year to June. Dwelling completions remain an issue, with a strained construction sector keeping a floor under both rent and purchase prices.”

Rent yield dynamics are also changing, which could shape future investor activity.

For the first time in the history of the CoreLogic gross rent yield series, Brisbane and Adelaide rent yields are on par with Melbourne, at 3.7%.

Gross rent yields in Perth are also showing a substantial decline, from a recent high of 4.8% in June 2023 to 4.3% in August.

“Yield compression is common when values are rising strongly, which may slow investor interest in high-growth cities. However, many investors are attracted to long-term prospects for capital growth over high rent returns.”

Looking forward, the national housing market should continue to see modest value increases to the end of 2024. While there is a clear slowdown in growth, housing values are underpinned by a longer-term lack of new supply, which has been exacerbated recently by ongoing constraints in the residential construction sector. The latest Statement on Monetary Policy from the RBA highlighted that finishing trades are in short supply, and the public infrastructure pipeline is creating greater competition for labour, especially in the multi-unit sector.

Buyer numbers have slowed amid high cost of living pressures, but vendors in most markets will likely be empowered to delay their home sale if buyers do not meet their price expectations.

Tight job markets continue to support mortgage servicing, however a more substantial loosening than expected in the labour market is a key risk for housing values.

Tax cuts and energy rebates are improving household finances but may not translate to a boost in home buying. The Westpac-MI consumer sentiment index rose 2.8% in August, buoyed by improved sentiment of household finances as stage three tax cuts kicked in, and the cash rate remained on hold for a sixth consecutive meeting. However, sentiment around dwelling purchases continued to decline.

“There is such a wide gap between an affordable home for the median income household in Australia and actual dwelling values that the impact of tax cuts is unlikely to substantially increase the number of buyers.”

CoreLogic puts the estimate of an affordable purchase price at about $500,000 for the median income household, against a median dwelling value of $802,000. This discrepancy has likely narrowed the buyer pool to wealthier and higher-income buyers.

Spring sellers should be aware of differences market-to-market. Heading into the spring selling season, there is no guarantee that buyer numbers will rise to meet the seasonal uplift in listings.

While total stock levels are generally low across the country, there are some markets where total listings are accruing despite soft price performance (mainly across Victoria and Tasmania).

In such a varied market, those looking to sell this spring should be conscious of local conditions, such as the number of properties currently on the market, the amount of time properties are taking to sell, auction clearance rates and price movements, before listing.

For a household earning $100,000 per year, an affordable purchase price would be $506,000 (assuming 30% of income on a mortgage with a 20% deposit, and average owner-occupier mortgage rate of 6.28%).

Source: Corelogic.com